Award-winning PDF software

Form 575E Wilmington North Carolina: What You Should Know

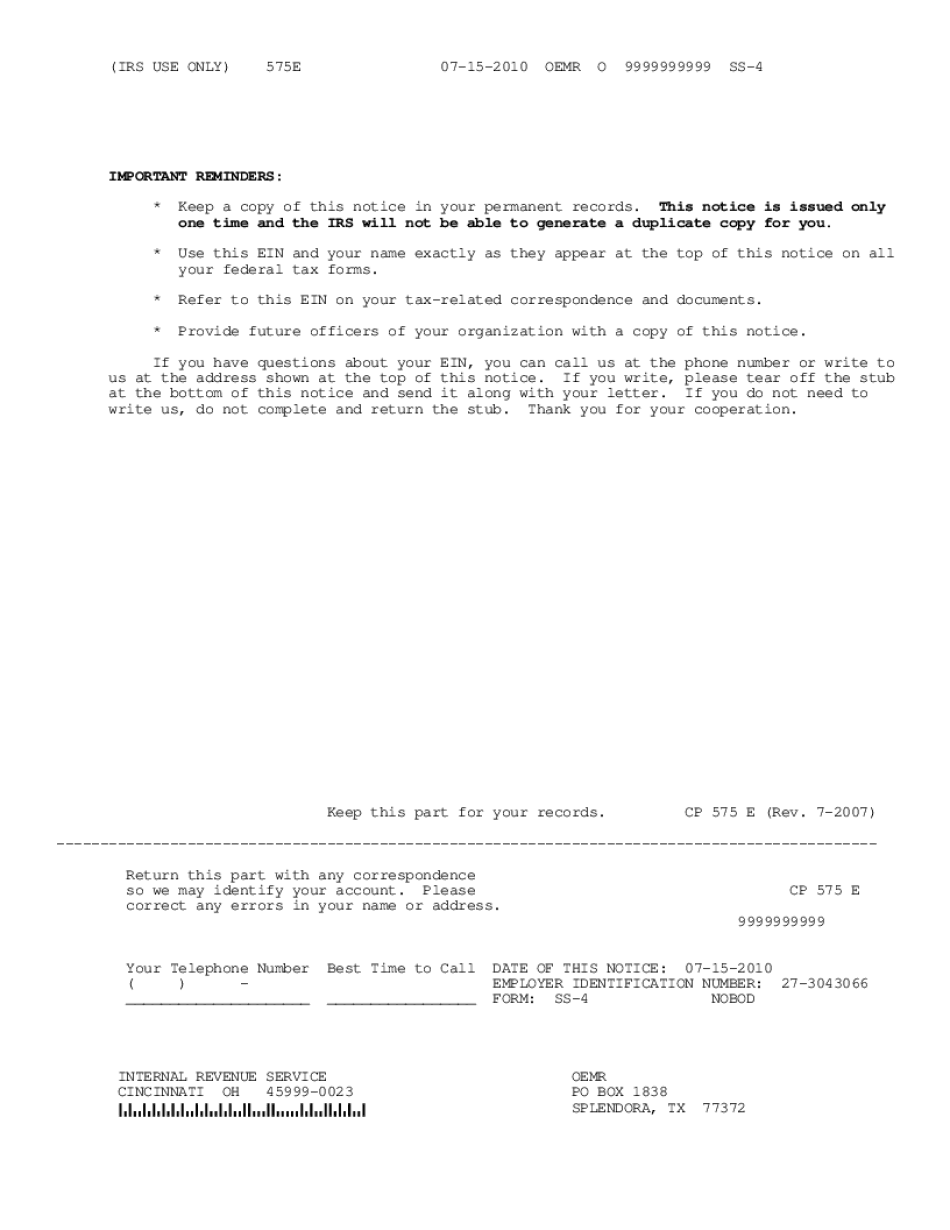

Filed by: J. J. Humboldt, II. Filed by: David H. Raiding, III, III. (Raiding, David) Petitioner files a notice of appeal with the Court of Appeals that an administrative fee collected by the Internal Revenue Service is tax-exempt. Petitioner Filed this civil action, on May 27, 2009, to collect an administrative fee previously owed to the United States by its predecessor corporation (Company A), a manufacturer of medical equipment. The administrative fee, which was due to the Internal Revenue Service and paid on November 12, 2008, was owed under the Internal Revenue Code section 704(a)(28) for failure to file an FAR prior to February 1, 2008. The District Court held that a failure to file an FAR would not constitute a failure to furnish information with respect to a U.S. person, if (1) the failure to file an FAR would not have materially affected the United States person's ownership interest in the entity, (2) due to extraordinary circumstances at the time of the filing of the FAR, the failure would not reasonably be expected to result in the inability of United States persons to dispose of the entities' interest after the date of the filing of the FAR, and (3) the filing was filed after the date of the enactment of the Foreign Corrupt Practices Act. The court also held that the failure to file an FAR could not result in the inability of United States persons to dispose of the entities' interest for five years after that date. On March 23, 2010, the court entered an order finding that the parties agree and recognize that the filing of an FAR under Title 26 of the Internal Revenue Code was required. The order also found that the failure to file an FAR resulted in a substantial risk that the United States persons would not have been able to dispose of the interests in the entities within five years of the filing of the FAR. However, the court found that the failure to file an FAR during the period of time between February 1, 2008, and February 1, 2009, was not substantial enough that the failure had the effect of materially impairing the ability of United States persons to dispose of the interests in the entities. On March 23, 2010, the court granted the IRS's request to stay the proceedings until the court issued its final decision as to the meaning of the term “material” for purposes of Title 26.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 575E Wilmington North Carolina, keep away from glitches and furnish it inside a timely method:

How to complete a Form 575E Wilmington North Carolina?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 575E Wilmington North Carolina aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 575E Wilmington North Carolina from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.